[From

Bjorn Simonsen (2004.02.18.15:00 EuST)]

[From Rick Marken (2004.02.04.1025)]

Ø

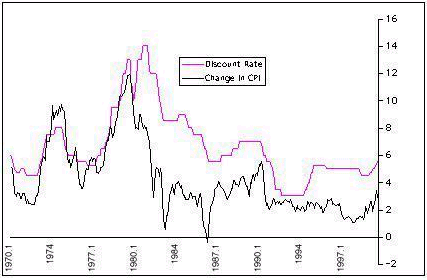

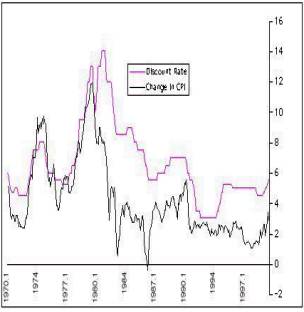

The result

shows what appears to be a clear positive relationship between

discount

Ø

rate and inflation rate, exactly the opposite of the relationship

assumed in popular

Ø

discussions of economic policy.

To the right you see the graph from

Norwegian data.

[insert

inflatedisc.jpg here]

The positive

relationship between discount rate and inflation rate shows up at nearly

all phase delays between

these time plots of these two variables. This is shown in the

lagged analysis in the

attached laginflatedisc.jpg. The lags/leads on the X axis are the

number of months by

which the discount rate leads (- values) or lags (+ values) inflation

rate. Discount rate

does not become negatively related to inflation until 22 months before

the inflation changes.

And the negative relationship is quite low. The negative relationship

between discount rate

and inflation never exceeds -.11, and that that level of negative

relationship doesn’t

occur until discount rate leads inflation by 36 months (3 years).

Compare this to the

very strong positive relationship (.59) between discount and inflation

rate that reaches a

maximum when discount rate follows inflation rate within 11 months.

Thank you for your answer in private mail

2004.02.11. I have till now spent some time on this thread and I will give you

some comments. I have collected the same data as you did and I have analysed

them in your way.

I don’t agree completely with your

formula “ ((CPI(t)-CPI(t-1))/CPI(t).) is the way the government

measures inflation rate”. I think divisor shall be CPI(t-1), because the change

is from time (t-1). And the formula

((CPI(t)-CPI(t-1))/CPI(t-1)). I thought that this should give growth

when you have decrease and reversed, but I can’t see any differences in my

graphs in contrast to yours. Maybe you have used ((CPI(t)-CPI(t-1))/CPI(t-1))

when you calculated yourself?

Here is

my graph where I show the Correlation coefficients phase leaded/lagged. It is Quite as yours.

image003.wmz (4.27 KB)

image005.wmz (2.07 KB)

image007.wmz (1.56 KB)

image009.wmz (2.23 KB)

image011.wmz (1.28 KB)

image013.wmz (6.28 KB)

image015.wmz (4.36 KB)

image017.wmz (4.37 KB)

oledata2.mso (305 KB)

···

To

the left you find my graph from US data. The graph is quite like yours of

course. To the right you see a different graph. Here is no negative data at

all.

Ø

………This results in the positive correlation between

discount and feedback when

Ø

discount follows inflation (positive lag values). But changes

in the discount rate seem

Ø

to be positively related to inflation (rather than

negatively, as assumed by the Fed) as

Ø

indicated by the positive relationship between

discount and inflation when discount

Ø

precedes inflation (negative lag values). This

positive feedback relationship between

Ø

the Fed chief’s actions and the results of those

actions on the controlled variable

Ø

inflation – would result in runaway inflation

if the Fed chie kept raising rates. But

Ø

the positive relationship between the Fed chief

actions and inflation seems to level

Ø

off after a few months. So runaway inflation is

prevented by the limit to the Fed chief

Ø

response to the inflation he has coaused causes by his

own actions.

I

think there is a positive

correlation between Discount

and the Inflation rate when the Discount is correlated with the Inflation rate some months before. But

the value is low, and it doesn’t tell us much.

Also I see the positive feedback between

the Discount and the effect on inflation and I think the Fed chief has

something to learn about negative feedback.

Ø

Increases in the Fed discount rate takes money out of

the economy, which should make

Ø

it difficult to get money for investment and growth.

My own visual inspection of the data

Ø

led me to the same conclusion: it looks like discount

rate and growth are negatively

Ø

related. But I wanted a quantitative measure so I got

the raw data and made my

Ø

own version of Canterbury’s Figure 14.2, which is the

graph is seen in growdisc.jpg.

Ø

I used the raw data (actually, I was able to get data

that went back to 1959, rather

Ø

than just 1975, but the statistical results are the

same for the 1959-2000 and for the

Ø

1975-2000 time period) to compute the actual

correlation between discount rate and

Ø

growth. And the results were a big surprise. It turns

out that the zero lagged correlation

Ø

between discount and growth is positive (.25). The

apparent negative relationship

Ø

between the discount and growth curves seen in

growdisc.jpg is actually an optical

Ø

illusion. The complete phase analysis of the

relationship between discount and growth

Ø

is shown in the graph in laggrowthdisc.jpg.

I did the same analyse as you and my graph

is quite like your laggrowthdisc.jpg. Below my graph.

But

my graph presents the Correlation coefficient for different Phase lags/leads

some different from your laggrowthdisc.jpg. My graph is below.

I

have tried to reanalyse my calculations and I shall do it again. I have used

the formula 100*(C21-C20)/C20 in Excel where the date in row 20 is lower than

the date in row 22.

But

both graphs indicate that

Ø

What this analysis shows is that changes in discount

rate that precede growth are

Ø

actually positively related to growth, a result that

is, again, completely the opposite

Ø

of what many economic policy experts seem to believe

is true. Increases in discount

Ø

rate are believed to lead to decreased growth. This

would show up as a negative

Ø

relationship between discount rate and growth when

discount rate precedes growth.

Ø

In fact, just the opposite is seen.

Yes

Ø

All the results presented here describe relationships

between variables that exist as

Ø

part of a closed loop system. I think the only way to

figure out what is actually going

Ø

on – that is, to figure out how variables like

discount rate, grwoth and inflation actually

Ø

influence each other – is to build closed loop models

and try to match the behavior of

Ø

the models (over time) to the observed behavior of the

variables observed.

I

have done it and I am a little excited.

I

used your model in [From Rick Marken (2004.02.07.2330)]

p = Discount in preceding month-Actual inflation rate in the preceding

month

Discount = Discount + 0.1 * ((0.01 * (0-p)) - Discount) *dt, where dt =1

month

Here you can see the graph showing the Inflation rate (upper graph) and

the Simulated Discount (lower graph)

I calculated the

Correlation coefficient between the data for same date, and it was 0.49. Then I

calculated a Correlation coefficient between the Inflation rate and the

Simulated Discount, the inflation rate for one month earlier than the Simulated

Discount setting. Here the

Correlation coefficient is 1,00. I guess you don’t believe it. Therefore I give

you a part of my calculations

I used the

formula output = output + 0.01 * (8 * (-p) -

output)

You used the

formula p = sim_discount (i-lag) -

dCPI (i-lag)

I used the

formula p = sim_discount - dCPI (i-lag)

CPI

Date

dCPI Simulated Discount

39,8

1970.12

0,50505051

0,45094052

39,8

1971.01

0

0,44866304

39,9

1971.02

0,25125628

1,5231E-07

40

1971.03

0,25062657

0,2232043

40,1

1971.04

0,25

0,2226449

40,3

1971.05

0,49875312

0,22208828

40,6

1971.06

0,74441687

0,44306874

40,7

1971.07

0,24630542

0,66130476

40,8

1971.08

0,24570025

0,21880619

40,8

1971.09

0

0,21826859

40,9

1971.10

0,24509804

1,5231E-07

40,9

1971.11

0

0,21773361

41,1

1971.12

0,48899756

1,5231E-07

The dCPI is calculated

as (A35-A34)/A34 ex. Line 3 an 4 (40-39.9)/39.9 = 0.25062657

And at line 4 I have

calculated the Simulated Discount as D35+0.001*(0.25*(0-(D34-C34))-D35). Here

the Correlation coefficient taken at the same date is 0.08. But if you Phase

displace one month the dCPI and the Simulated Discount 1 month later you get a

Correlation coefficient at 1.00. Try it.

I have worked with a

simulated Discount using your formula “output = output + 0.01 * (8 * (-p) -

output)” on Norwegian data. The graph below shows the Norwegian Inflation rate

and a Simulated Discount.

I calculated the

Correlation coefficient between the data for same date, and it was 0.20. Then I

calculated a Correlation coefficient between the Inflation rate and the

Simulated Discount, the inflation rate for one month earlier than the Simulated

Discount setting. Here the

Correlation coefficient is 1,00. I guess you don’t believe it. Therefore I give

you a part of my calculations

Here I used the same

formula you used output = output + 0.01 * (8 * (-p) -

output)

CPI

Date

dCPI Discount Change of Simulated Change of the Discount

The Discount

64,5

1986M03

0,78125

13,37

-1,32841328

0,278648555

64,9

1986M04

0,62015504

13,65

2,09424084

0,694444444

65

1986M05

0,1540832

14,36

5,2014652

0,551248923

66,1

1986M06

1,69230769

14,31

-0,34818942

0,136962849

66,8

1986M07

1,05900151

14,58

1,88679245

1,504273504

67

1986M08

0,2994012

14,56

-0,13717421

0,941334678

68

1986M09

1,49253731

14,46

-0,68681319

0,266134398

68,3

1986M10

0,44117647

14,6

0,96818811

1,326699834

68,5

1986M11

0,29282577

15,02

2,87671233

0,392156863

68,8

1986M12

0,4379562

16,4

9,18774967

0,260289572

69,8

1987M01

1,45348837

16,34

-0,36585366

0,389294404

70,5

1987M02

1,00286533

15,09

-7,6499388

1,291989664

The dCPI is calculated

as (A35-A34)/A34 ex. Line 4 an 5 (40-39.9)/39.9 = 0.25062657

And at line 5 I have

calculated the Simulated Discount as F20+0.01*(8*(0-(F20-C19))-F20). Here the

Correlation coefficient taken at the same date is 0.00. But if you Phase

displace one month, the dCPI and the Simulated Discount 1 month later, you get

a Correlation coefficient at 1.00. Try it.

I will show you a wonderful

figure from my Norwegian data.

This is how the

Norwegian Bank (Norwegian FED) would like to see the graph of the Inflation

rate and the Change of Discount.

The Correlation

coefficient with 1-month phase shift is –1.00, telling me that their action with the discount is exact

opposite the Inflation rate. When the inflation rate grows they choose a

Discount with correct effect.

I don’t believe this

is true. I have tried to extricate myself and find where I do something wrong. But

I don’t find it. So I am asking for comments.

Have a nice weekend.

bjorn