Martin Lewitt (2010.02.20.1634 MST)

[From Rick Marken (2010.02.21.1000)]

Bill

Powers (2010.02.21.0635 MST)

Martin Lewitt (2010.02.20.1634 MST) –

Time series data are often autocorrelated. Your independent variable

(tax policy changes) only changes a dozen or so times, presumably there

is a time lag analysis you should do and then test whether the amount

of time between changes is enough for the dependent variable to fully

respond. The statistical significance of your correlation should be

reduced by the amount of the auto-correlation.

I think Rick probably knows this, since he has taught statistics and

experimental methods (including writing a book on the latter).

Thanks, but I don’t like to point to my credentials as evidence that I

know what I’m doing. After all, we know that credentials, such as a PhD

in psychology, don’t guarantee that one has not wasted one’s career

pursuing an illusion.

As to Martin’s point about autocorrelation, I think your comments to

Martin are most pertinent:

I

don’t quite see what you’re getting at here – you seem to be arguing

on Rick’s side by agreeing that there are no data favoring the idea

that reducing taxes increases growth; all you’re saying is that the

evidence indicating the opposite is not as strong as it might seem to

be. That doesn’t show that decreasing taxes increases growth.

Exactly. The fact is that even by assuming that the sample points in

the tax and growth time series are independent (independence and

autocorrelation are actually two different things; more on that later)

the correlations were not (except in a couple cases) statistically

significant. As you say, reducing the number of degrees of freedom for

the statistical test, as Martin suggests based on the fact that the

series is autocorrelated, simply makes all the correlations not

statistically significant, which makes my point: I can find no evidence

for the claim that lowering taxes is associated with an increase in

growth.

As to autocorrelation and independence, these are actually two separate

concepts. A time series of data points can be independent and have a

high level of autocorrelation or they can be dependent with a low level

of autocorrelation. The former is probably rare; the fact is that

economic time series have a high level of autocorrelation and the

events are not independent. But it is possible for a series of data to

have a high level of autocorrelation while the events in the series are

actually independent. For example, you could have 100 people rate how

much they would pay for a bet where the payoff varies sinusoidally from

the first to last person. The series of 100 ratings will probably vary

sinusoidally as well, and a sine wave has a very high level of

autocorrelation, of course. Yes the data points in both the payoff and

rating series are independent of one another, in the sense that the

payoff or rating for subject n was independent of the payoff or rating

for subjects n-1, n-2, etc. And example of data where there is a low

level of autocorrelation and a high level of sequential dependence

would occur if the same study were done with the same person making all

100 ratings. In that case, it is highly likely that the rating that the

subject gives on trial n would depend on the ratings given on trial

n-1, n-2, etc.

But all this is really irrelevant to what I was trying to show. I use

correlations as a summary measure of the relationship between time

series, where on variable in the time series can be considered the

independent variable in a quasi-experiment. I could just present the

time series for visual inspection, since that is often the way the

results of quasi-experiments are reported. But it’s simpler to report a

correlation, which summarizes (in terms of fit to a linear model) the

relationship between IV and DV in this quasi-experiment using a single

number. I presented the rather small, positive correlation between

taxes and growth not to show that taxes cause growth; the relationship,

significant or not, doesn’t show that; we need a model to understand

why the data behave as they do. I presented the data as a question: why

the heck do economists think that increasing taxes reduces growth?

It is the microeconomic changes in behavior from increasing taxes.

I think what is most amusing about Martin L’s criticisms of my analysis

is that he makes so statements to which his criticisms actually apply.

Beside his complaint about my improper calculation of statistical

significance, Martin’s also complains about the “uncontrolled

confounding factors are easy to point out”. In fact, I look at time

series data in order to minimize confounding (the is what

quasi-experimental design is about, the idea being that it is unlikely

that other variables will be systematically confounded with time

variations in the variables of interest – like taxes and growth - if

these variables are looked at over a long period of time).

So I am well aware of the possibility of confounding and make every

effort to minimize the possibility in my economic analyses. But when

Martin talks about what he considers data he evidences absolutely no

concern about possible confoundings. For example, Martin says: “The

boats being lifted [by US tax cutting policies] are huge new middle

classes in India

and China and the world is better for it”. So Martin has no problem

attributing causality to the one co-occurrence of US tax cuts and the

growth of the middle class in China and India, ignoring all the other

events (possible confoundings) that occurred in US and the world the

same time.

I think several phenomena are being conflated here. The reasons the

boats being lifted are in China and India rather than in the US are

more complex than mere tax cuts in the US. Yes, it took economic

growth to lift those boats, but India and China did have some

comparative advantages in labor costs and regulatory environment, and

US taxes were still relatively high even after tax cuts, and of course,

free trade and globalization policies also assisted in allowing the

transfer of productive activity to India and China. When someone is

engaging in nationalist rhetoric and demagoguing the rich as arguments

for a more coercive policy, I don’t need rigorous statistical proof for

these things. I merely need to weave a plausible alternative

explantion of the facts. The evidential standard for proposing

freedom rather than coercion is lower.

Another example of Martin’s ability to do without

quasi-experimental control of possible confounding variables occurs in

the following analysis:

“The aim [of the tax cuts] was economic efficiency and growth.

Complicating matters is

that the Federal Reserve, which is supposed to be neutral in the

allocation of the returns from increased productivity between labor and

capital, took sides. By considering increases in wages inflationary

and tightening, it saw to it that nearly all the benefit of increased

productivity went to capital. The Repubs and Democrats were both

stupid in not recognizing and correcting this. The double taxation of

returns to equity and high tax rates also decreased the attractiveness

of the US economy as a place for investiment”.

Again, Martin is able to tell that the reason the tax cuts were not

associated with the intended results (lifting all boats) was the Fed

raised rates. Of all the many events going on in the US at this

particular time Martin is again able to tell (without the help of

quasi-experimental control) that Fed rate increases trump the effect of

tax cuts.

The fact is that Martin L. doesn’t seem to care all that much about

data. I think most free-marketers don’t care about or even like data

very much. Why would they? When the data contradict everything you

believe about economics then one of the best policies is to ignore it.

That’s just basic PCT.

Once again, all I have to do is weave a plausible alternative story.

I’m not proposing coercive measures. The plausible alternative serves

two purposes, it points out that the coercive policies may not be

needed, and it subtly shows how poorly understood the economy is, so

that even if there is a crying “need” for the coercive policy, there is

the real possibility that it may not have the desired effect, but even

the opposite effect instead. Everything else being equal, raising

taxes increases revenues, but everything else isn’t equal is it? Not

only do taxes taken from the rightful owners preclude what those people

would have done with the money, the taxes result in other changes in

behavior.

I admit, the nonlinear nature of the economy works both ways. While

my hope is that my proposal to eliminate the double taxation on

dividends combined with capping the deductability of interest will

result in more equity financing and lower levels of leverage in the

economy, the preference for borrowing rather than sharing ownership may

be so great that even more economic activity gets transferred to for

favorable environments.

If the Democrats want to suck the productive elements of society dry,

then they must take a lesson from the USSR and prevent them from

escaping while they still have any juice in them. While the USSR went

to the extremis of armed guards, barbed wire and mine fields, the

Democrats must, at least, oppose free trade and globalization.

You

also seem to be sidestepping another point made by Rick: he said

“Several times in recent years I have seen statistics showing that for

the last century or so each time the ownership of all the country’s

resources owned by the top 1% of the population has increased until -

with the latest one I’ve seen (within the last year) - it has reached

over 80%.”

This actually was said by Dick Robertson. It seems like an incomplete

sentence. I think Dick’s point was that “each time a large share of

ownership goes to a small share of the population the economy goes into

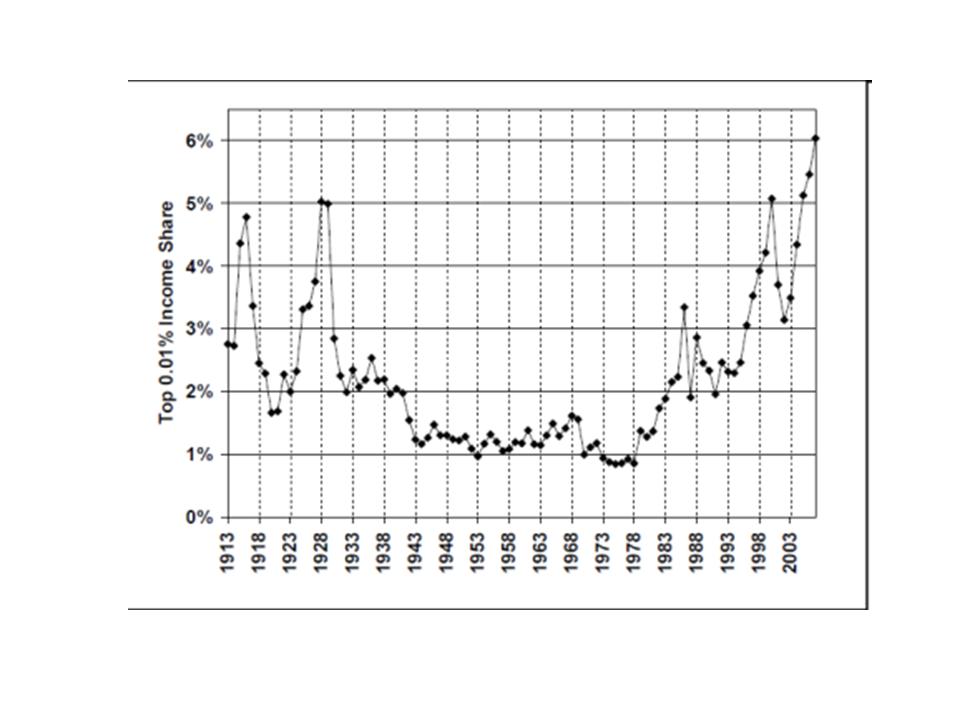

a dive”. I would say this counts for income as well. I’m attaching a

graph of the share of GDI (gross domestic income) going to the top .01%

of the population of the US. Note how the share of income went up (to

5%) right before the Great Depression, then after decreasing to 1% and

staying there for a long time it took off again starting as soon as

Reagan came into office. The graph peaks out again (at 6%) right before

the second great depression of 2008-2009. Coincidence? I don’t think so

It may not be a coincidence. Depressions may hit the extremely rich

particularly hard, or recessions may turn into depressions, because the

top 0.01% get demonized and their wealth confiscated, or the wealthy

get shamed into philanthropy instead of continuing productive

activities. Certainly there is a natural human tendency for

politicians to blame others than themselves. Were there no government

or federal reserve policies that contributed to the concentration of

wealth? I’ve already pointed some out.

Humans have to deal with a complex nonlinear environment often with

only fuzzy incomplete local information. Perhaps our tendency to

develop moral rules and simplified principles and models had adaptive

benefits in such environments. Perhaps they have no predictive value,

just persuasive value? I’d like to think there is value to

generalizing from simplified micro-economic models, but there may not

be. I do like freedom, and appreciate that at least a plausible case

can be made that it works better than coercion.

Democrats like to distort the market in ways that create perverse

incentives, and then blame the people for following those incentives

off a cliff. Even the simple models we already have, predict such

results, although market resiliance makes the timing of the predictions

notoriously bad, sometimes off by a decade or more.

Martin L.