[From

Bjorn Simonsen (2004.02.23,17:30 EuST)]

[From

Rick Marken (2004.02.21.0930)]

[From

Rick Marken (2004.02.22.1040)]

Could you do me a favour and send me

(in a spreadsheet) the Norwegian data on gross

private investment and growth in GDP (or GNP) going back as far as you can go.

(I got back to 19653). I used quarterly data but I’ll take what I can get. What

I

would like is real (not inflation adjusted) GDP (or GNP), inflation adjusted

GDP (or GNP)

and real (not inflation adjusted) gross private investment (I don’t think they

report

inflation adjusted investment, I presume because they assume it will be

measured

as a proportion of GNP, which would also have to be in real dollars). If you

can get

me gross government investment as well that would be great (in the US they

report

defence and domestic investment as separate parts of government investment).

I

send you private the spreadsheets-You will find 1) The Norwegian data Grossed

fixed capital formation at current price, Ip, General government

investment (Ig), and the GDP. The data is partial quarterly data and yearly

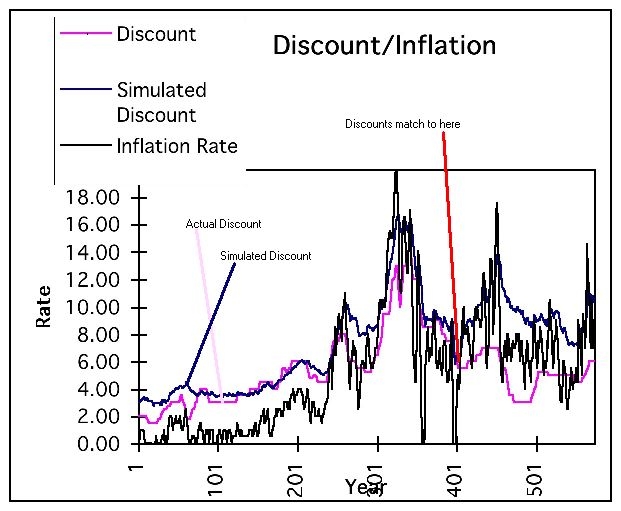

data. And 2) a Norwegian CPI table 3) A Simulated Change in Discount and

Correlation coefficients and 4) An Analysis of Norwegian Discount relative to

CPI.

If

any other is interested, give me a mail

I

don’t know if it is

.

…a wonderful birthday present (my birthday is next Saturday, 2/28).

But,

Happy Birthday. I shall have my birthday on Friday 2/27, and I leave the same

day for our cottage in the mountain.

I am back again Monday.

Did you do these calculations using

Visual Basic? In my calculations, the value of

sim_discount that is used in the

calculation of p is the value of output calculated

on the prior iteration of the following

loop (lines stating with an apostrophe are remarks.

If

you go to 3) A Simulated Change in Discount and Correlation coefficients and

4) An Analysis of Norwegian

Discount relative to CPI you will see that the calculations are very simple. I

have just made the formulas in a cell and dragged the Cell in accordance to the

CPI and the date columns. You will understand when you open the spreadsheets.

I

know you use Visual Basic, but I think functions in the spreadsheet also work

well.

If

you look at 3) A Simulated Change in Discount and Correlation coefficients you

see I still get the correlation coefficient like 1. In the same spreadsheet you

will see that I have not used your formula for the output

F16+0.01*(8*(0-(F16-C15))-F16),

I have used = F16+$D$8*($D$9*($D$10-(F16-C15))-F16).

I

have substituted 0.01 with $D$8 and substituted 8 with $D$9 and your reference

0 with $D$10. This is Simply and

you have maybe done it yourself. I thought it was exciting having a Simulated

Discount graph and changing the values in D8, D9 and/or D10. Then I could see

how the graph changed when I clicked F9.

I

didn’t understand your comments about my correlation coefficient =1.00. If you

see a mistake, please tell me.

I

did the same wit the US Simulated Discount data. And I got the Correlation

coefficient almost =1.00 also there.

I see that you did do an analysis of

Federal Gross Investment and Discount Rate

(something I did not do). Was this for the

Norwegian data? If so, then you can

apparently get the data I want: Norwegian

Gross Federal and Gross Private

Investment as well as Norwegian Real and

Inflation Adjusted GDP.

I

did it also with the US data. I send it to you as 5) US Investment relative to

Discount

bjorn

···