Economic Data Analysis

[From Rick Marken (2004.02.04.1025)]

Here are some more data analyses that I did some time ago to test some popularly held ideas about how the economy works. One such idea is that the Fed discount rate can be used to control inflation. The discount rate is used to influence the amount of money in circulation. Increasing this rate takes money out of circulation.

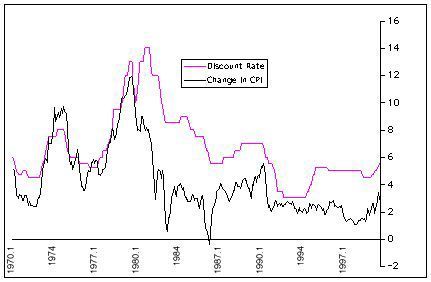

Apparently under the theory that inflation results from too much money in circulation, many economic policy makers believe that the Fed can tame inflation by raising the discount rate. A couple of years ago I went to the FRED data site and got the discount rate and CPI (consumer price index) data that was available. What I got was monthly measures of these two variables from 11/1970 to 5/2000, 354 data points. I derived inflation rate from the monthly CPI values and found the results shown in the inflatedisc.jpg attached. The result shows what appears to be a clear positive relationship between discount rate and inflation rate, exactly the opposite of the relationship assumed in popular discussions of economic policy.

[insert inflatedisc.jpg here]

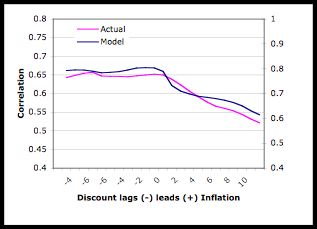

The positive relationship between discount rate and inflation rate shows up at nearly all phase delays between these time plots of these two variables. This is shown in the lagged analysis in the attached laginflatedisc.jpg. The lags/leads on the X axis are the number of months by which the discount rate leads (- values) or lags (+ values) inflation rate. Discount rate does not become negatively related to inflation until 22 months before the inflation changes. And the negative relationship is quite low. The negative relationship between discount rate and inflation never exceeds -.11, and that that level of negative relationship doesn’t occur until discount rate leads inflation by 36 months (3 years). Compare this to the very strong positive relationship (.59) between discount and inflation rate that reaches a maximum when discount rate follows inflation rate within 11 months.

[insert laginflatedisc.jpg here]

The results of this analysis suggest, to me, that discount rate may be controlled (the control system doing the controlling being Greenspan) relative to inflation rate in a positive feedback control loop. That is, it look like Greenspan (or whoever the Fed chairman is) raises rates when inflation goes up and decreases rates when inflation goes down. This results in the positive correlation between discount and feedback when discount follows inflation (positive lag values). But changes in the discount rate seem to be positively related to inflation (rather than negatively, as assumed by the Fed) as indicated by the positive relationship between discount and inflation when discount precedes inflation (negative lag values). This positive feedback relationship between the Fed chief’s actions and the results of those actions on the controlled variable – inflation – would result in runaway inflation if the Fed chie kept raising rates. But the positive relationship between the Fed chief actions and inflation seems to level off after a few months. So runaway inflation is prevented by the limit to the Fed chief response to the inflation he has coaused causes by his own actions.

I think that’s the correct interpretation of the results in laginflatedisc.jpg. But I will run some simulations to check it out.

By the way, after producing the graph in inflatedisc.jpg from the raw data I found exactly the same graph in Canterbery, E. R. (2000) Wall street capitalism, River Edge: NJ, World Scientific. Canterbery’s book was pointed out to me because it makes considerable reference to the work of TCP. Anyway, if you get the book you will see that his Figure 14.1 (p. 266) is exactly equivalent to the graph I made that is shown in inflatedisc.jpg. And Canterbery comes to the same conclusion as I do about it: the observed relationship between discount rate and inflation is exactly the opposite of what many economic policy experts think it is.

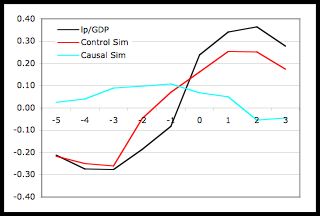

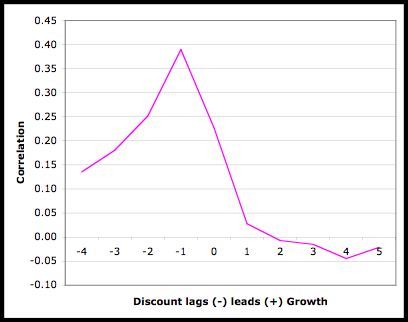

Canterbury also looked at the relationship between Fed discount rate and economic growth. He presents his results in Figure 14.2, p. 269. That graph looks about the same as the one in growdisc.jpg, attached below.

[insert growdisc.jpg here]

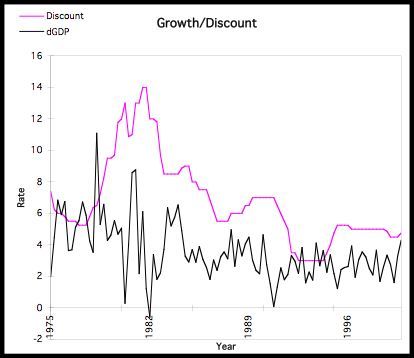

Apparently based on the visual appearance of this graph, Canterbery concluded that there is a negative relationship between discount rate and growth, which is, again, the relationship that is believed to exist between discount rate and growth by many economic policy experts. Increases in the Fed discount rate takes money out of the economy, which should make it difficult to get money for investment and growth. My own visual inspection of the data led me to the same conclusion: it looks like discount rate and growth are negatively related. But I wanted a quantitative measure so I got the raw data and made my own version of Canterbury’s Figure 14.2, which is the graph is seen in growdisc.jpg. I used the raw data (actually, I was able to get data that went back to 1959, rather than just 1975, but the statistical results are the same for the 1959-2000 and for the 1975-2000 time period) to compute the actual correlation between discount rate and growth. And the results were a big surprise. It turns out that the zero lagged correlation between discount and growth is positive (.25). The apparent negative relationship between the discount and growth curves seen in growdisc.jpg is actually an optical illusion. The complete phase analysis of the relationship between discount and growth is shown in the graph in laggrowthdisc.jpg.

[insert laggrowdisc.jpg here]

What this analysis shows is that changes in discount rate that precede growth are actually positively related to growth, a result that is, again, completely the opposite of what many economic policy experts seem to believe is true. Increases in discount rate are believed to lead to decreased growth. This would show up as a negative relationship between discount rate and growth when discount rate precedes growth. In fact, just the opposite is seen.

All the results presented here describe relationships between variables that exist as part of a closed loop system. I think the only way to figure out what is actually going on – that is, to figure out how variables like discount rate, grwoth and inflation actually influence each other – is to build closed loop models and try to match the behavior of the models (over time) to the observed behavior of the variables observed.

Best

Rick