···

-----Original Message-----

From: Control Systems Group

Network (CSGnet) [mailto:CSGNET@LISTSERV.UIUC.EDU] On Behalf Of Bill Powers

Sent: Sunday, 30 December 2007

2:21 a.m.

To: CSGNET@LISTSERV.UIUC.EDU

Subject: Re: Indifference curves

[From Bill Powers

(2007.12.29.0404 MST)]

Gavin Ritz (2007.12.29.16.39)

Money is

not a good in the sense that it can be used for a specific purpose (s) (like a

motor car, or a computer) it is a special good in that it is the only good that

qualities (what is valued) can be converted into quantities (but never

perfectly) as qualities can never be fully defined especially in the sensual

sense.

If we want to apply PCT to economics, we have to be prepared to junk everything

that people (and especially we ourselves) love and think they know about

economics. This means that we have to be explorers, not defenders or attackers.

Economics has largely been defined by people with a stake in the way things

are, which means that bad logic and missing or non-factual facts are overlooked

as long as an argument gets these people to the conclusion they wanted in the

first place. The usual conclusion desired is “There is nothing wrong with

the way I (or we entrepreneurs) do things.” I think we should avoid promoting

such conclusions before we know they are true.

You say (if I interpret your sentence correctly) that money allows quality (of

goods) to be translated into quantity (of money).

What I’m

saying is not the quality of goods but a quality (essence, property, or value ie

a quality), is translated to quantity. So the quality can be beauty, or just

some functional quality.

Does

it really do that?

Yes it’s

the only thing we have that does that. Money is named after the goddess of prosperity

Moneta, and

ancient money endowed a certain god like quality. It obviously still does many

people still believe money is their god, although they may not admit it.

Before

we can follow your ideas any further, we have to know whether thi s

statement is true; if it’s not true, we would be wasting our time by assuming

its truth and going on to explore its implications, since conclusions that

depend on its truth can’t be used to prove its truth. One inconvenient fact

could bring the whole structure of ideas down if you leave any large loopholes.

One

first has to interpret the specific meaning of my statement before anything

like this can be done.

David Friedman, in his Price Theory, says that money is

the common measure of all value, which I take to mean something like what you

mean by quality. But he can’t define value any more than you can define

quality.

Of course

we can’t define quality and value which have similar endowments.

PCT,

on the other hand, offers definitions of both terms, but they wouldn’t please Friedman.

Economists

wanted to be seen as physicists, which of course is plain silly.

The

value of a good, we might say on the basis of PCT, is the reference condition

of a higher-order perception that is a function of the (perception of owning

the) good. For example, the value of a railway ticket is found in the intention

to get off the train in some other place where one wants to be. It is a

higher-order variable that is controlled, in part, by purchasing the ticket.

I think

you make it way too complicated, in PCT you can simply say it’s the intrinsic

error.

Friedman would not like this definition partly because it implies

that one railway ticket is enough, and two would be too many. He is not willing

to admit that there can be enough of any good.

Well

there’s no end ever to any sensual quality and values, that’s what

creates the weaving and un-weaving of our societies ad infinitum.

Friedman would not like this definition also because it implies

that a good can have two different values at the same time.

I can’t

say, but what I can say is that economics has many flaws in it and many economists

know that hence many of them are looking at other avenues for exploration like Brian Arthur.

Buying

the railway ticket not only serves the purpose of getting you to your

destination, it also keeps you from being accosted and embarrassed or even

arrested for trying to travel without a ticket. It also provides you with a

receipt in the form of a punched and dated document showing that you could not

possibly have committed a certain murder. It may also go into your scrapbook

showing that yet another in a set of notable train trips has been ticked off

your list. It could conceivably accomplish all these ends at the same time.

Unfortunately, that means that the ticket could be placed on intersecting

indifference curves, and indifference curves are not supposed to intersect. If

they can intersect, one rather elaborate economic house of cards will collapse.

Yes, but

its ultimate purpose

is to get one from A to B, which is driven by another need, ie the reason one wants

to be at B, a holiday, a conference, visit family or whatever.

Human

process-structures (infrastructure) like a railway system have one primary purpose

and that is to “connect” far flung property so that they can

communicate in all manner of things. (goods, services, communication-postal, protection,

holidays etc)

PCT shows how multiple perceptions at one level can EACH contribute to multiple

higher-order perceptions, so that there are multiple scales of value, not just

one. Since there is no one measure of value inside a person,

That I believe

is correct, I have a commercial psychometric tool (I combined the content and

process theories of motivation) called IVA which stands for internal value analysis. And the combinations of values

(qualities) and behaviours are in the order of billions.

My

instrument actually measures the intrinsic error which is really just a tension

gap.

it

follows that there can be no one scale of value outside the person that is

representable by money. Money, therefore, cannot measure value. It i s

simply a token that can be exchanged for goods, by common consent.

Yes you

are correct it does not measure value in the sense like an instrument, it

exchanges value. If you take it away we just barter, you can endow the value in

a cockle shell or a cow, money is just a very convenient method of exchange. Money

is a converter and exchanger of value or a quality.

The

value of what is received in return for the money depends on context.

Doesn’t

everything always depend on a context? The sound of my wife’s footsteps

in my home is different to the sound of footsteps of enemy soldiers I would

encounter in a war context.

A

railway ticket that can save me from the electric chair is worth a lot more to

me than the same ticket needed to fill a blank space in my scrapbook today

rather than next week.

The Mastercard commercial on TV says it all: there are some things that money

can’t buy; for everything else, there’s Mastercard. Even in the

“everything else,” however, what money can buy by way of value varies

a lot even for the same good. The last superbowl ticket is worth more than the

first superbowl ticket to be sold, even if the seats are side by side or the

buyers trade seats. The Reading Railroad is worth lots more if you already own

the other three on the Monopoly board, though its price (if not already bought

by another player) doesn’t change because of that. In fact, if there weren’t

some very good reason for wanting to say that value = money, one might not find

it too hard to discover endless examples to the contrary. It all depends on

whether you’re trying to prove that money can measure value, or are a teeny bit

skeptical and just want to know if it really can.

Money is

a currency if one has a very bad human organ (genetically damaged) no amount of

money can replace it (at this point in time anyway). But money can never equal value that means they are one

and the same which of course they are not, money converts qualities to quantities.

Money is

like the bell as in Pavlov’s dog’s bell. The ringing of the bell makes the dogs salivate for their food,

not the food. It’s a representation.

As does

human work. Which we can exchange for money, of course never perfectly.

Regards

Gavin

=====================================================================

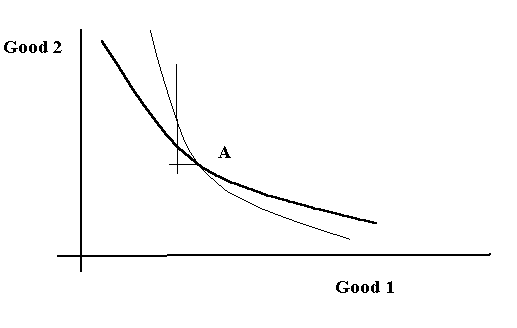

Rick, and anyone else involved here, I suggest that we start by

looking at “marginal utility.” If an increment of some good is worth

more when there are fewer of the good in possession, the implication is that

the more goods you get, the less the “value” of the next increment

will be (the less you will be willing to spend to get more). This idea is used

to predict that indifference curves will be convex toward the origin. But a lot

depends on just how the marginal utility declines as the quantity of the good

increases.

If the decline follows a curve like a negative exponential, it is possible that

the desire for more will not ever entirely disappear, though it may get quite

small for very large amounts of goods already in hand. But it is possible that

the decline is such that the desire for more goods goes to zero at some finite

amount of goods, and reverses sign after that. In that case, we have a control

system with a reference condition that defines “enough” of the good,

as well as “not enough” and “too much.”

We have to remember that all statements about supply and demand apply to

populations, not individuals, and that individual characteristics can be quite

different from population characteristics. When we say that marginal demand

decreases gradually as the amount already purchased increases, we do not mean

that in each individual the decrease is gradual. It is possible that each

person acts as a high-gain control system with only a narrow range of goods

over which the effort to get more drops to zero and goes negative. But in a

population, the exact amount of goods at which the drop in demand starts will

be distributed around some mean with some standard deviation, and the standard

deviation will determine how gradual the aggregate change in demand appears.

In fact it is quite possible that over the population the reference levels for

goods follow a distribution like the Poisson, which tails off exponentially. In

a large population, this would lead us to expect that no matter how high the

desire for goods, there will always be a few individuals who desire even more.

Such outliers might even have a very specific idea of how much

“enough” is (say, all the railroad companies west of the

Mississippi), but since there are so few of them they simply contribute to a

decline in marginal utility for the population that looks as if it will never

reach zero. This could lead to the false impression that the human agent always

wants more, when in fact every human agent has a definite idea of

“enough”.

So I think PCT and common sense lead to some serious doubts about Friedman’s

assumptions. If he is right in saying that he is merely informing us about

“How economists think” and is not espousing some oddball deviation

from normal economics, I think we can conclude that normal economics needs some

fairly drastic revisions.

Best,

Bill P.