[From Frank Lenk (2009.09.12.13:21 CDT]

I ran across an article today

in Real World Economics Review (warning: this is a heterodox economics journal)

**Efficient market theory vs.

Keynes’s liquidity

theory ** 85

Paul Davidson download pdf

In it, Davidson makes the following point, which I thought had

relevance for a PCT based model of the economy:

Taming uncertainty in Keynes’s liquidity theory

For decisions that involved potential large spending outflows or

possible large income inflows that span a significant length of time, people

“know” that they do not know what the future will be.

Nevertheless, society has attempted to create institutions that will provide

people with some control over their uncertain economic destinies.

In capitalist economies the use of money and legally binding

money contracts to organize production and sales of goods and services

permits individuals to have some control over their cash inflows and outflows

and therefore some control of their monetary economic future. Purchase

contracts provide household decision makers with some monetary cost control

over major aspects of their cost of living today and for months and perhaps

years to come. Sales contracts provide business firms with the legal promise

of current and future cash inflows sufficient to meet the business

firms’ costs of production and generate a profit.

Note that in this view, money is not just some other good to be

exchanged. It, plus legally binding contracts denominated in money, is

the mechanism by which we achieve our economic reference signals.

Yes, we could write barter contracts, but as Davidson says

later:

Money is that thing that government decides will settle all

legal contractual obligations. This definition of money is much wider than

the definition of legal tender which is “ This note is legal tender for

all debts, private and public”

An individual is said to be liquid if he/she can meet all

contractual obligations as they come due. For business firms and households

the maintenance of one’s liquid status is of prime importance if

bankruptcy is to be avoided.

Hence, people hold money (as savings) in times of uncertainty

(which all times are really, though we seem to forget this as a society

after times have been good for a while). They hold money so that even in the

face of economic disturbances (even planned ones like college for the kids) they

can continue to maintain their reference signals. If they don’t

have the money, they take on debt to acquire it.

Money, then, has special properties, the chief one being

that it is the most liquid of all assets. As such, it is that asset that most

easily enables people to control their economic lives (although if they take on

too much debt, they will quickly find they lose in the long run what they

gained in the short run),

At least, that’s my interpretation of money and PCT. I’d

be interested in hearing others’.

Frank

···

From: Control Systems

Group Network (CSGnet) [mailto:CSGNET@LISTSERV.ILLINOIS.EDU] On Behalf Of Bill

Powers

Sent: Monday, September 07, 2009 1:18 PM

To: CSGNET@LISTSERV.ILLINOIS.EDU

Subject: Re: [CSGNET] economics

[From Bill Powers (2009.09.07.0945 MDT)]

Frank Lenk (2009.09.06.20:32 CDT] –

FL: Well, Bill, since you’ve thrown down the gauntlet,

I guess I need to reply.

WARNING: About 2/3 of the proposal is actually a

review of the urban sociology literature. The problem I (ultimately) want to

solve is concentrated poverty among minorities in urban areas (affecting mostly

African-Americans in Kansas City, but also Latinos). The model I am hoping

develop is merely a tool for understanding more clearly the nature of problem

and the effectiveness of proposed solutions. I think PCT and agent-based

modeling give me the best chance of developing such a tool.

BP: I think so, too. I hope you’re aware of the recent book by McClelland and

Ferraro, “Purpose, Meaning, and Action,” which is about using PCT in

sociology.

[http://www.amazon.com/Purpose-Meaning-Action-Theories-Sociology/dp/1403967989

](http://www.amazon.com/Purpose-Meaning-Action-Theories-Sociology/dp/1403967989)I’ll go over the draft dissertation in more detail, but there are a couple

of points to make.

The main one for now is the idea that reference levels originate in the social

system. I think this is a simple mistake, and one reason why the model of

individuals has to be kept in mind. A reference level is simply a particular

state of a perception that has been selected as a target or goal. A cruise

control works that way: when the driver pushes a button, the current

speedometer reading is stored as a reference signal, which then serves to

specify the speedometer reading that is to be maintained. The driver, a

higher-order control system, pushes the button when satisfied with the current

speed.

Each person has perceptions of various aspects of society. Society exists only

as the set of all individual perceptions of it (where else could it be?).

People may learn to use similar words to refer to social variables (like

“respect”), but those words often point to very different

perceptions.

from interacting with people, individuals determine which results of social

interactions they like or don’t like, and set their reference levels for the

social variables they perceive accordingly. They control those social variables

(or try to) according to the way they see them, not the way other people see

them. The mistake old-time sociologists made was to assume that the society

they saw was the same one that the individuals in it saw. I think your model

might benefit from acknowledging that what a suburban researcher sees as

“urban core decline” might be quite different from what a resident of

the urban core sees. This might make the behavior of such a resident more

comprehensible to the researcher. It might be that the resident sees the

“decline” as part of someone’s effort – maybe his own – to make

life better.

FL: I should also say that, while I did not know him, Bill

Williams was a professor at my school, the University of Missouri-Kansas City

(UMKC). I was introduced to PCT by a colleague of his, Dr. Jim Sturgeon.

BP: I remember Bill’s talking about Jim Sturgeon, who helped Bill achieve

recognition that he despaired of ever getting. It’s good to know that Sturgeon

was spreading the word about PCT, too.

FL: The major difference in my approach from Bill

P.’s, at least as I see it, is that I am doing the modeling at a couple

of levels below the economy itself. I understand the need for simplicity

– In trying to explain what I am doing to others, I have often to said that

I would be satisfied if I produced decent model of a family, let alone an

entire economy or society. But in our search for starting simple, Bill

and I are starting in different places. I would like to model at the

level of, not just individuals, but individuals who interact with each other

within families and communities. I want a model that starts from their

basic (intrinsic) needs and has the economy emerge from their social

interactions and the interactions with the available technology (which I would

have to specify).

That’s actually the same level I want to get to, but I’m starting with a model

that initially takes into account only the mechanics of the economy: buying and

selling, working and earning. The next step is a similarly low-level model of

the producers and their plants. All agent-based, of course – nothing happens

just because it happens. Then I would start getting into questions of why the

reference levels for the lower-level perceptions are set one way rather than

another. Because I am not an economist, I have to take small steps, and would

expect that at some stage real economists would get impatient and say

“Move over, let me do that.” I would happily comply.

As I said in my earlier post, one can view the economy as

simply a set of behaviors we use to control the amount of food in our bellies,

subject to certain environmental constraints. My conception of the environment

includes the social as well as the natural and the technological,

however. I want my agents to figure out how to organize themselves to

live in the virtual world inside my computer, much as we have had to figure out

how to organize ourselves to live in this one.

You’re just talking about higher-level organizations than I am starting with.

To me, social aspects of the economy boil down to what individuals think the

society is and should be, which in turn come from their experiences with it

(including what others tell them about it). The only way these higher-level

systems can work, however, is through adjusting the reference levels for the

systems I am trying to model first.

There are several reasons for my wanting to model at this

level. First, I think that the only human behavior we truly understand is

that which we experience, which is that of ourselves and small groups of others

with whom we regularly associate. This is the level at which we have any

expertise to specify our model. Our common, every-day experience provides

the data we need to begin, though ideally this would be checked against results

from psychology, anthropology and sociology.

OK, I agree that families are a good place to start, being a finite unit with

not too many interactions. In my approach families would enter initially only

as dependents – drains on the store of goods and services which breadwinners

work to pay for. I don’t mean they’re resented for that – that’s a matter for

higher levels of control. I just mean they have that effect.

Second, human behavior is always in reference to others.

Under all but the rarest of circumstances, there is no such thing as an

isolated individual living alone. We depend upon others for our most basic

needs - for food, for sex and parenting of offspring to

reproduce. A model that begins with its “atom” an

isolated individual is likely to produce a different outcome from one that

specifies interactions between individuals from the beginning (perhaps a

mother-child relationship is the atom of social models).

Don’t worry about that part of it, it will be added once the foundation is

laid. At the level where I’m considering the model now, reference signals are

simply variables and we can look at the consequences of adjusting them. We can

introduce more people, and see the consequences of different combinations of

reference levels being sought in a common environment. This doesn’t commit us

to any particular reference settings; it just says that if you set them this

way, that is what will happen. Then, of course, we have to try to test

that prediction with data.

Obviously, to get interacting individuals one has to

start by identifying, specifying and debugging the control systems inside a

single individual, but those control systems should be built to perceive others

and let others influence the individual’s references (learning by

emulation or mimicry, for example) and perceptions (or at least what is

important to perceive).

Yes, and this is my intention once the lower levels are taken care of. Though I

think references are acquired in a way somewhat different from what you assume

(I maintain that children learn perceptions and references mainly by watching

what adults do and interacting with them, not by listening to what they say).

And anyway, we don’t just “learn references.” We learn to adjust

references in real time for lower systems as a means of controlling

higher-order variables. Reference signals are normally variable according to

actions initiated at higher levels and disturbances that tend to alter

higher-level perceptions. We don’t just “set and forget” references.

Third, and this is especially important given my problem of

concentrated minority poverty, once we allow others to influence either our

references or our perceptions (and probably both), the notion of Power rears

its head. Who influences whom and how? There is much evidence that, at

least partially, we set our references according to the behavior of those more

powerful than we. This is certainly true of a child. It also probably

accounts (again, at least partially) for the transmission of stereotypes, roles

and norms.

I think our references and perceptions grow out of social intereactions not by

imitation so much as by resisting disturbances. What we take away from social

interactions is mainly what we learned to do to maintain control, not what we

saw the other person doing. In some cases, of course, a child sees something

another person is doing, and says “I could do that!” But the actual

learning comes from the doing, not the watching. A great deal of what is

learned (for example, from being abused) is what one has to learn to maintain

control of one’s own life.

So in my proposed approach, the economy is behavior we

engage in to control the food, shelter and water we need to survive while we

engage in other behavior to control for the other things that are important

(perhaps more important) to us – mating, parenting, gaining social

position or esteem. Clearly, these purposes are inter-related – one

who controls the resources for food and shelter also becomes powerful and

desirable as a mate and a parent. Some (many?) will argue that gaining

esteem or social position is really all about maximizing potential for mating,

so in this sense is only a behavior to control for mating probability or

frequency rather than a reference. I tend to think that while this may

have originally been the case, humans and their antecedents have been social

creatures long enough that some hardwiring of an intrinsic need for belonging

to a group or being valued by the group is likely.

Isn’t it simpler to assume that what is hardwired is a desire for certain

consequences of belonging or being valued? Those desires are satisfied in

different people by different behaviors, sometimes by opposite behaviors –

which accounts for the low correlations one gets in any study aimed at finding

universal behavior patterns. Some people like being with other people all the

time; some people like a lot of time alone. It’s not the behaviors we care

about, it’s the consequences they produce. Some might say that people learn to

make fires in order to imitate others who made fires. I say they learned to

make fires because they want to stay warm.

Reading through Bill’s approach again, I think it is

clear that it is simpler and more achievable more quickly than mine. But

one of the things I uncover in my survey of the agent-based modeling literature

is that the models are very sensitive to assumptions, especially about what the

rules are that the agents follow.

Yes, indeed. And those rules are variables or adjustable features in my model.

I check out rules to see how they work, but anyone can plug any rules they like

into the same model to see what happens. For example, in the model I sent you,

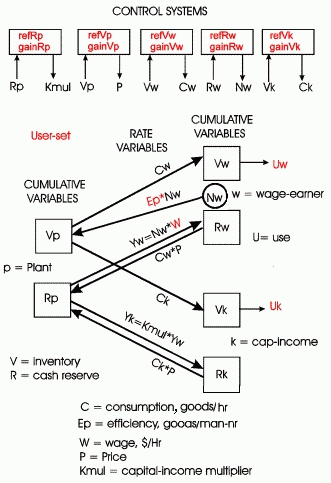

a plant manager keeps inventories at a fixed level by adjusting prices. That

works quite well and gives a reasonable law of supply and demand, but maybe

there are other ways of doing the same thing. You can substitute the other

ways, or you can add more plants and managers and see what happens when

different managers work according to different rules. Maybe some rules lead to

going out of business. Others may generate conflicts.

In PCT terms, where do our references actually come from? If

they are simply assumptions made by the modeler, they will be subject to

criticism. Some are intrinsic, yes. But the rest? We must learn them. We likely

learn them as kids, both from experience and from others. So let’s model

the learning process in families and groups of families and see what kind of

economy we can derive from members’ efforts to satisfy their needs.

Fine, the reorganization algorithm has been checked out in systems of up to 500

interacting control systems. It ought to work with four or five people

controlling 10 or 20 variables. But you do need a starting point – an

underlying architecture of control systems to provide parameters that can be

reorganized.

My strategy in general is to model control systems and leave their detailed

properties to be determined. Where I assume reference levels to test the model,

I want to substitute higher-order control systems to adjust them once the lower

level is working right. Where I assume particular controlled variables, anyone

is free to propose other controlled variables. Ditto for means of action. The

only reason for making particular assumptions about the lower-level systems is

to make sure they will work, and to learn what they can do.

Best,

Bill P.