[From Bill Powers (2009.11.18.1221 MDT)]

Martin Taylor 2009.11.18.10.36] –

It’s interesting that you have a

problem with your control analysis that is analogous to my problem with

the (probably) artifactual uniformity of the mean error averaged across

objects within SS# bands. I have no answer to either, at the

moment.

I think the explanation is clear now. A straight line of data points will

correlate with another straight line even though the slopes are

different, which is why correlations are useless for fitting models to

data. I’ve now changed the program so it adjusts the reference level and

gain to get the best values of gain and reference by minimizing the RMS

difference between the real and modeled “output” variable,

which is just Asked - Bid price. The optimized values of gain and

reference are used for both the bids and the outputs. The optimization is

repeated 10 times, going back and forth between gain and reference

adjustment. That achieves perhaps a 10% reduction in RMS error relative

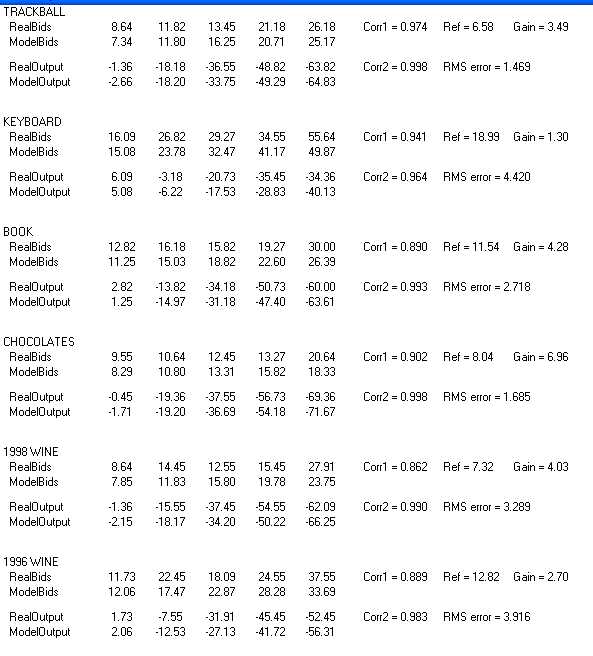

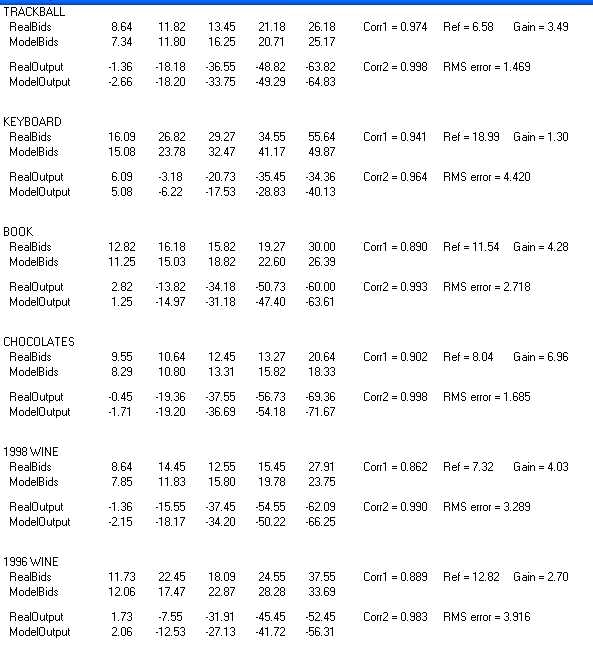

to a single iteration. Here is the table of results (it’s a jpeg graphic,

a cropped screen shot, also attached):

As you can see, the RMS error between RealOutput and ModelOutput is

reasonably small; for the Keyboard row, which has the largest RMS error,

it;'s about 11% of the maximum output (4.4 out of 40). The correlations

(Corr2) range from 0.983 (worst) to 0.998 (best). I’ve attached the final

version of the AriellyUn Unit, where all the calculations are shown. It

just produces the table above, so is of interest only to programmers who

can read the pascal code. Not commented much, I’m afraid. I’m about

burned out on this for the time being.

Best,

Bill P.

AriellyUn2.pas (6.22 KB)